The Euro like many great but complicated projects has different storylines. There are the simple versions for general public consumption and what politicians find to be useful sound-bites that are difficult to challenge technically, and then there are the more complex deeper reasons that risk technical arguments beyond the capacity of most politicians to master and that are therefore deemed suspiciously suspect because they are above the capacity of the public to usefully (politically) understand. The consequence is policies promoted for misleading even spurious reasons.

The Euro like many great but complicated projects has different storylines. There are the simple versions for general public consumption and what politicians find to be useful sound-bites that are difficult to challenge technically, and then there are the more complex deeper reasons that risk technical arguments beyond the capacity of most politicians to master and that are therefore deemed suspiciously suspect because they are above the capacity of the public to usefully (politically) understand. The consequence is policies promoted for misleading even spurious reasons.The reasoning that led to creation of the Euro and its support system the Growth & Stability Pact (also known as The Maastricht Criteria) had a number of political motivations including closer integration picture-framed by a few simple practical ideas for the public to understand such as easier cross-border trade and savings for tourists on currency conversion costs.

The most important reasoning however was really to create a currency too big to be played with to the extent of its credit being severely damaged by the markets, a currency that would not suffer the blackmail of the markets as in the case of Sweden and the Nordic currency crisis of 1991-3, The ERM crisis of 1992-3, the Sterling crisis (termed "Black Wednesday") of September 1992 (and of some importance the Latin American currency crises of the late '80s and Mexico in 1994-5 and East Asian in 1997-9).

The most important reasoning however was really to create a currency too big to be played with to the extent of its credit being severely damaged by the markets, a currency that would not suffer the blackmail of the markets as in the case of Sweden and the Nordic currency crisis of 1991-3, The ERM crisis of 1992-3, the Sterling crisis (termed "Black Wednesday") of September 1992 (and of some importance the Latin American currency crises of the late '80s and Mexico in 1994-5 and East Asian in 1997-9). The first paradox therefore is that clearly the money markets have in fact been able to discredit the Euro system to such an extent that like the earlier ERM with its narrow bands it is struggling to survive. If it falls apart, partly or wholly, market speculators have a golden opportunity to make short term large gains by shifting in and out of different Eurozone countries' equities, bonds and currency holdings.

When the Euro was created (January 1, 1999) and in the months leading up to this date the money markets lost 10 interest rates, currencies and bonds differentials to trade in and out of. A lot of markets liquidity was lost and investment banking gross trading profits of several hundred $billions a year. Money had been made by aggressive speculators in the ERM (also known as currency snake) years. The essential ingredient facilitating successful speculation (including short-selling)is a rigid system with transparent rules that can be easily tracked by the markets. The narrow bands within which currencies within the ERM were allowed to move were manna to the speculators.

The second paradox therefore is that in creating the Euro to be resistent to market speculators it was furnished with rigid transparent rules in terms of maximum ratios of budget deficits and of gross national (government) debt as a % in ratio to GDP. In the first years of the Euro a certain latitude was permitted including in the case of the largest economy of the Eurozone, Germany.

Following a brief Eurozone technical recession in 2008 (a shock response to the international Credit Crunch) it was obvious that the next speculative opportunity would be loss of confidence in soverign debt as measured by the Euro's ratio rules. Such sovereign debt crises have always been triggered after a recession when governments increase their budget deficits and national debts in order to pull their economies out of recession.

Following a brief Eurozone technical recession in 2008 (a shock response to the international Credit Crunch) it was obvious that the next speculative opportunity would be loss of confidence in soverign debt as measured by the Euro's ratio rules. Such sovereign debt crises have always been triggered after a recession when governments increase their budget deficits and national debts in order to pull their economies out of recession.That this should be especially a problem for the Eurozone and Euro system was easily predicted by many experts, though ignored and voted down at several IGCs. The Delors Plan and European Recovery Plan both of which advocated a trillion Euros to smoothe differences between economies netering the Euro was voted down by Germany, Netherlands and UK when supported by all others. Germany and UK especially were adamently opposed to brussels getting its hands on such a large spending reserve.

The markets speculators have merely had to wait for the Euro's first important recession to test its structure. The experts doubted how any currency could be sustained through and after a severe economy downturn if it is not directly supported by government finances. The Euro was only supported by the European Central Bank whose flexibility is constrained and whose ability to respond to some countries problems more than others is politically and constitutionally limited.

Brussels economists planning for the Euro in the mid-1990s told me privately that they believed The Maastricht Treaty was too simple and too inflexible. But because of the political drive behind the Euro it would be a disaster to drop the Euro plan, a disaster to delay it, and a disaster to proceed with it! The politicians and others had painted themselves into a tight and unsustainable corner.

It was hoped that after five years of low growth and higher unemployment against trend caused by The Euro's introduction that lessons would be learned and a more sophisticated system introduced. Such a system should take better account of different GDP growth paths of each national economy, allowing for some that were growing based on heavy bank lending to property thereby causing trade deficits and those were growth was predicated mainly on export surpluses and therefore on banking lending to industry.

It was hoped that after five years of low growth and higher unemployment against trend caused by The Euro's introduction that lessons would be learned and a more sophisticated system introduced. Such a system should take better account of different GDP growth paths of each national economy, allowing for some that were growing based on heavy bank lending to property thereby causing trade deficits and those were growth was predicated mainly on export surpluses and therefore on banking lending to industry. In the first decade Greece for example was praised year after year for contributing to Eurozone GDP groth much above its weighting in the Eurozone economy. It did not matter that Greece ran up the biggest trade deficit in the OECD relative to its GDP. Current account (external) payments balances were not part of the Maastricht Criteria. Ireland benefited to from excessive praise. While its GDP seems to be growing fast because of its massive trade surplus relative to GDP, the fact that it had huge current account payments deficits (uniquely so) was ignored! The system of rules was too simple.

When the ECB and other central banks set interest rates there are rules and obligations at work. But they are flexible; matters of judgement that make the interest rate decisions very difficult for the markets to predict and to successfully speculate against. This ambiguity in how decisions are arrived at and what they mean is a very useful policy tool that became evacuated from the Eurozone, especially so once Germany (with alongside other net exporters) was no longer in breach of the ratio rules.

During the Credit Crunch (not yet over) banks and later governments that refinanced their banks using government bonds (not bills i.e. on-budget, not off-budget) the great anxiety was to bring down the cost and raise the certainty of supply of loans to banks (to recycle their funding gap finance) and to governments (to keep borrowing costs in line or below that of the rate of GDP growth and of government revenue growth).

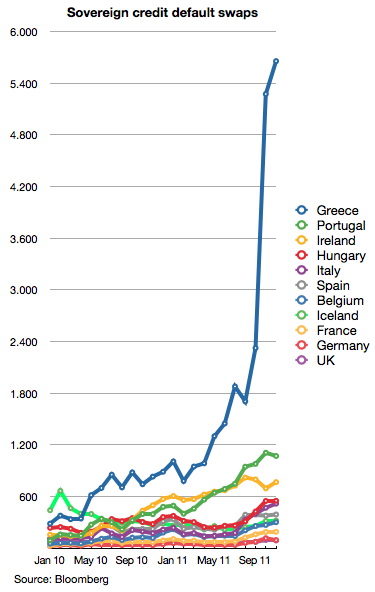

During the Credit Crunch (not yet over) banks and later governments that refinanced their banks using government bonds (not bills i.e. on-budget, not off-budget) the great anxiety was to bring down the cost and raise the certainty of supply of loans to banks (to recycle their funding gap finance) and to governments (to keep borrowing costs in line or below that of the rate of GDP growth and of government revenue growth). German banks and the banks of net exporters (also called competitive economies) are heavily exposed to industry where lending margins are tightest and herefore their cost of borrowing is most critical to banks' profitability and solvency. As those competitive countries could appear so much "stronger" than deficit countries in the politics of the European Sovereign Debt Crisis their cost of borrowing would fall slightly as the deficit countries such as Greece especially found their cost of borrowing soaring. This is a vicious beggar-my-neighbour strategy. And this alone is enough to severely discredit the Euro Project and the prospects of its sustainability.

The third paradox is therefore that a Euro system intended to integrate surplus and deficit countries works only when there is growth and appears to fall apart when there is recession! It is failing the essential solvency test that of surviving intact over a whole economic cycle.

The third paradox is therefore that a Euro system intended to integrate surplus and deficit countries works only when there is growth and appears to fall apart when there is recession! It is failing the essential solvency test that of surviving intact over a whole economic cycle.With the Euro Sovereign Debt Crisis the European Central Bank that was created to be free of political interference has been displaced spectacularly by the central role in financial structuring taken by leading politicians, by the leaders of the "major powers" in Europe. This is a fourth paradox. It is linked to a sixth paradox that the European Union of equals regardless of size has morphed into a Union where the largest players dictate the economics of the smallest players.

This in the case of Greece reminds us of the Munich Agreement of 1938 that dictated the dismemberment of Czechoslovakia without the Czechs at the bargaining table! The European Community, European Union and Eurozone predicated on European integration for the avoidance of war ever again is risking precisely again political disunity and potential for cross-border and civil war violence and possibly military or comparable dictatorships. This is the seventh paradox that financial and trade integration to make war (or near warlike disputes) impossible is now the single biggest factor in Europe's disunity.

This in the case of Greece reminds us of the Munich Agreement of 1938 that dictated the dismemberment of Czechoslovakia without the Czechs at the bargaining table! The European Community, European Union and Eurozone predicated on European integration for the avoidance of war ever again is risking precisely again political disunity and potential for cross-border and civil war violence and possibly military or comparable dictatorships. This is the seventh paradox that financial and trade integration to make war (or near warlike disputes) impossible is now the single biggest factor in Europe's disunity.In part it is the mindfulness of this that prompts Merkel and Sarkozy and others to seek tighter integration through fiscal unity and more rigid deficit and debt rules. They hope the amrkets are appeased by a rigid common order. But, we have plenty of experience to show us that transparant rigidities in the system encourage aggressive speculation.

It is repeated often that Germany above all fears currency collapse as in 1923. It has a practical fear certainly of a high Deutschmark destroying its trade surplus if the Euro system collapsed and the Eurozone members returned to each having a floating national currency. But, in 1923 the German currency was destroyed by short-selling speculators precisely because it was confined within a rigid system of enforced war reparations payments and dollar shortages. There was no flexibility allowed until it was too late.

That the Merkel-Sarkozy proposals and the austerity measures enforced on Greece and Ireland and others are foolishly based on increasing the rigidity of the rules and that takes us further deeply into all the paradoxes above.

That the Merkel-Sarkozy proposals and the austerity measures enforced on Greece and Ireland and others are foolishly based on increasing the rigidity of the rules and that takes us further deeply into all the paradoxes above. Aplying the rules will become even more severe and untenable if the crisis after Austria then more severely engulfs major economies Italy and Spain! The markets will not let up; they cannot so long as the liklihood of worsening crisis persists. It will do so for additional reasons. The Eurozone is in the early period of its normal recession, a recession only to expected that is on schedule to anyway regardless of the Euro Crisis as macro-economists can predict this merely based on past history!

Once Germany cannot politically sustain keeping within the bounds of the Maastricht budget deficit ratio perhaps only then will the Euro system be allowed to become more intelligent and more flexible! The sooner the better for all.

It is a political problem of the first order in the wake of the Credit Crunch and Banking Crisis and the various austerity programmes for politicians to be seen advocating any solutions however sensible that sound like "funny money" or "painless" or gaming the system by allowing flexible responses. The mistrust of the voters and their cynicism and anxieties currently are boundless. It will take politicians of truly major statesmanlike stature to explain a truly Communitaire policy response and be believed involving cross-border trust and everyone sharing the blame, burdens, and the rewards according to financial need and not merely according to economic size. A relaxation of the rules and more flexibility in their interpretation plus more sophistication and complexity can supply a relatively painless solution for Europe and the world.

It is a political problem of the first order in the wake of the Credit Crunch and Banking Crisis and the various austerity programmes for politicians to be seen advocating any solutions however sensible that sound like "funny money" or "painless" or gaming the system by allowing flexible responses. The mistrust of the voters and their cynicism and anxieties currently are boundless. It will take politicians of truly major statesmanlike stature to explain a truly Communitaire policy response and be believed involving cross-border trust and everyone sharing the blame, burdens, and the rewards according to financial need and not merely according to economic size. A relaxation of the rules and more flexibility in their interpretation plus more sophistication and complexity can supply a relatively painless solution for Europe and the world.