The Euro Area and the Euro System are in trouble as much from speculative attack by the money markets as from the natural difficulties of getting countries with very different growth stances of a mix of severe surpluses and deficits to share a common currency. It cannot expect all its legs to move at the same time together in the same way and in the same direction, not how any animal system walks or runs.

The Euro Area and the Euro System are in trouble as much from speculative attack by the money markets as from the natural difficulties of getting countries with very different growth stances of a mix of severe surpluses and deficits to share a common currency. It cannot expect all its legs to move at the same time together in the same way and in the same direction, not how any animal system walks or runs. The EU needs a system of financial rebalancing that recognises the often extreme differences in each state's growth strategy and that accepts the inevitability of economic cycles. The Euro system rules are too simple and too rigid and offer the markets easy targets in the first recession testing of the Euro system.

The current system focuses on GDP only (not GNP) and fails to take account of payments external account and focuses on gross government debt (not net debt).

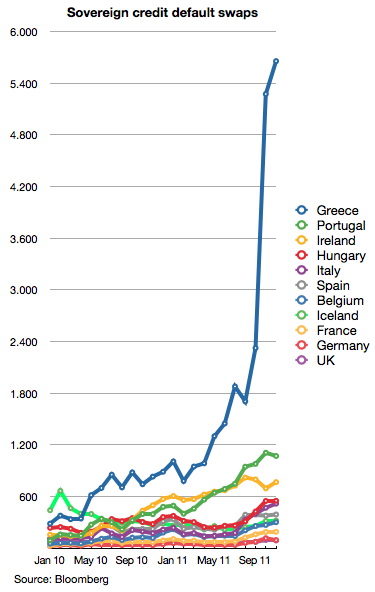

Greece and Italy are not the same problem except superficially. The EU and Euro Area are inevitably economies with opposing growth settings; export-led such as Germany (with banks focused 60% on lending to industry), deficit-led such as Greece and Spain (banks focused 70% on lending to property), or in rough external account balance such as France and Italy (where bank lending has been too conservative). Ireland is a unique mix of highest trade surplus and equally high payments deficit, which is bizarre? It has the highest trade surplus ratio to GDP and yet similarly high payments deficit. This shows it to be more a regional economy within the Uk than a truly national economy with its own domestic and national financial integrity.

Germany has a trade volume and export surplus equal to that of China. In the EU export surplus countries are equal to two times China. The rest of the bloc has to cope with this. Greece allowed itself to follow the examples of USA, UK, Ireland in growing GDP powerfully based on boom in mortgage lending. The banks were deaf to the entreaties of the Central Bank to stop that and lend more to industry.

The central problem is not national debts and who these are owed to. Nor is it that the banks cannot be profitably financially helped by governments over time. It is certainly partly the banks' fault for the dysfunctional pattern within each country of their domestic lending bias. But the politicians are not aware how to address that or that they have the powers through EU laws based on Basel II to do so?

The central problem is not national debts and who these are owed to. Nor is it that the banks cannot be profitably financially helped by governments over time. It is certainly partly the banks' fault for the dysfunctional pattern within each country of their domestic lending bias. But the politicians are not aware how to address that or that they have the powers through EU laws based on Basel II to do so? There are technical and definitional problems such as the simplistic Maastricht ratios. These should be termed funny money issues rather than levels of debt, which are well within the EU's financial resources to comfortably cope with over time.

The problem for all Euro Area governments is that when they provide financing loans to their commercial banks they have to do so on-budget and on-balance-sheet because their central banks no longer have treasury bill issuing rights. The USA and UK had no such problems and could insulate taxpayers from the refinancing of the banks.

When member states adopted the Euro it meant that T-bills (debt of 1 year or less maturity) that were previously issuable by central banks now gave up that power to the ECB. Today, countries in the Euro Area only issue T-bills from the Treasuries and debt management agencies and the debt therefore appears on budget (deficit) and on balance sheet (gross national debt). The UK and others can issue T-bills through their central banks where the debt is off-budget and off-balance sheet of the government. This provides immense flexibility to UK and others not in the Euro to provide financing to the banking system without directly embarrassing their budget deficits and national debt levels, a luxury denied to Euro Area governments.

IS GERMANY AT FAULT? Merkel has in 2008 and in the years since including this year done and said no other than say Margaret Thatcher would have done and said in the same circumstances. One difference is the quality of Finance Minister and Schauble is not allowing himself to overstep a nationalist line. There is a concern to advertise Germany as safe, successful and superior so that German banks can continue to rely on getting cheapest funding, cheaper than other EU member states' banks. But those banks are heavily over-long on lending to exporting industry that is in severe pain to service its debts. Export surpluses, the principal source of Germany's GDP growth, are not won cheaply! There has come a point in time now when to ratchet down any further on the PIIGS ability to fly will rbound negatively, even catastrophically, on the German economy and the solvency of its banks. If Merkel and her team can see this danger they may start to give more credence publicly to reforms in the Euro system that permit less rigid adherence to simplistic fiscla rules. For the moment, however, the talk is of more rigidity not less and that means rich pickings for financial arbitrageurs and currency shorters, whose pay day is coming soon with the imminence of a full-blown Euro Area recession! Only when Germany has to loosen its own financial constraints it may agree for other member states to do the same? The present disparities will soon result in financial arterio-schlerosis spreading throughout the Euo Area system whereby many more states will find their wholesale finance cost rising and higher funding costs hitting all banks. A bout of recession will markedly worsen this and governments will then have to get together and realise that they have to act in concert and expand their spending and borrowing.

IS GERMANY AT FAULT? Merkel has in 2008 and in the years since including this year done and said no other than say Margaret Thatcher would have done and said in the same circumstances. One difference is the quality of Finance Minister and Schauble is not allowing himself to overstep a nationalist line. There is a concern to advertise Germany as safe, successful and superior so that German banks can continue to rely on getting cheapest funding, cheaper than other EU member states' banks. But those banks are heavily over-long on lending to exporting industry that is in severe pain to service its debts. Export surpluses, the principal source of Germany's GDP growth, are not won cheaply! There has come a point in time now when to ratchet down any further on the PIIGS ability to fly will rbound negatively, even catastrophically, on the German economy and the solvency of its banks. If Merkel and her team can see this danger they may start to give more credence publicly to reforms in the Euro system that permit less rigid adherence to simplistic fiscla rules. For the moment, however, the talk is of more rigidity not less and that means rich pickings for financial arbitrageurs and currency shorters, whose pay day is coming soon with the imminence of a full-blown Euro Area recession! Only when Germany has to loosen its own financial constraints it may agree for other member states to do the same? The present disparities will soon result in financial arterio-schlerosis spreading throughout the Euo Area system whereby many more states will find their wholesale finance cost rising and higher funding costs hitting all banks. A bout of recession will markedly worsen this and governments will then have to get together and realise that they have to act in concert and expand their spending and borrowing.  Germany's economy appears to be externally strong (large export surplus as the main motor of GDP growth) but internally it is potentially weak. The banks are vulnerable by having loaned too much to industry (which is paying 10% of value added to service bank debt compared to only 10% of profit in case of UK industry, a nearly tenfold difference!).German banks are desperately in need of cheapest wholesale money (to support narrow margins and cash-flow based collateral) hence the hard attitude against deficit countries' fiscal problems - just a way of making Germany look good to wholesale finance providers relatively by comparison. If external trade shrinks and or becomes less profitable to exporters and if the Euro Area breaks up then Germany faces domestic economy meltdown (worst of all if it returns to a strong and soaring Deutschmark). The Euro Area is in any case now into its recession, a recession that follows as it usually always does 2 years after USA/UK recession. (EU/EA's brief recession in 2008 was not the real thing, only a shock from the financial bank crisis).

Germany's economy appears to be externally strong (large export surplus as the main motor of GDP growth) but internally it is potentially weak. The banks are vulnerable by having loaned too much to industry (which is paying 10% of value added to service bank debt compared to only 10% of profit in case of UK industry, a nearly tenfold difference!).German banks are desperately in need of cheapest wholesale money (to support narrow margins and cash-flow based collateral) hence the hard attitude against deficit countries' fiscal problems - just a way of making Germany look good to wholesale finance providers relatively by comparison. If external trade shrinks and or becomes less profitable to exporters and if the Euro Area breaks up then Germany faces domestic economy meltdown (worst of all if it returns to a strong and soaring Deutschmark). The Euro Area is in any case now into its recession, a recession that follows as it usually always does 2 years after USA/UK recession. (EU/EA's brief recession in 2008 was not the real thing, only a shock from the financial bank crisis). EU politicians have to learn again to kiss their European frog and trust it will turn into a prince again. The USA (Tim Geithner etc.) has very right to criticise the Euro Area politicians for being too reluctant to act in the interest of the whole international community - but he may be foolish to do so publicly. The same may be said of the UK's David Cameron. The Fed, Bank of England and the ECB have a joint responsibility for world money markets and when these seize up they have to intervene jointly. Foreign politician's criticisms - brickbats flung across the Atlantic or across European borders - are usually for domestic political consumption. It is easy to make broad statements but they only make sense when there are concrete ideas to be shared of how best to resolve the problems practically.

EU politicians have to learn again to kiss their European frog and trust it will turn into a prince again. The USA (Tim Geithner etc.) has very right to criticise the Euro Area politicians for being too reluctant to act in the interest of the whole international community - but he may be foolish to do so publicly. The same may be said of the UK's David Cameron. The Fed, Bank of England and the ECB have a joint responsibility for world money markets and when these seize up they have to intervene jointly. Foreign politician's criticisms - brickbats flung across the Atlantic or across European borders - are usually for domestic political consumption. It is easy to make broad statements but they only make sense when there are concrete ideas to be shared of how best to resolve the problems practically.It would be a reasonable accusation that the Euro Area fiscal rules are inflexible and simplistic. The Euro had its political supporters but technically was supposed to protect by sheer size against FX-money market speculators. The ECB was set up but placed in a constrained position and consequently fails to sufficiently compensate for the central bank powers that each Euro state gave up to the ECB.

Even the economists internally within the Euro planning teams in Brussels a decade ago foresaw this present disaster. But, back then, they hoped that after the first 5 years new more refined rules and better understanding of the technicalities would have evolved.

This didn't happen for various reasons most of which are political cowardice in face of global FX-money markets - mistakenly believed to be somehow most astute about economics and anyway ultimately all-powerful. The actual dysfunctional nature of information in these markets and their miserable irresponsible short term profit seeking etc. is all beyond the understanding of politicians and even of most political-economists, many of whom get little real-world model-building experience. The bankers also are afraid of economists and refuse to let them into the boardrooms where they fear that economists might take over - preferring instead to deal with the mathematical geeks whose understanding of risk cannot go further than market prices, rating agency ratings, and poorly cultured algorithms.

Must a new Euro system be legislated? The default direction of travel here currently among EU politicians is to seek a tighter union and tighter rules with a fiscal policing agency. But, practical reality dictates that the EU and Euro Area need less rigidity not more. The Euro sovereign debt crisis is a product of rigid rules and crude definitions of national debt. It is the rigidity that makes it an easy target for shorting speculators.

Must a new Euro system be legislated? The default direction of travel here currently among EU politicians is to seek a tighter union and tighter rules with a fiscal policing agency. But, practical reality dictates that the EU and Euro Area need less rigidity not more. The Euro sovereign debt crisis is a product of rigid rules and crude definitions of national debt. It is the rigidity that makes it an easy target for shorting speculators.The irony of the present situation is that the Euro was constructed to protect all members from money market speculators employing rumor-mongering of exaggerated insolvency scares. It is extremely damaging with incalculable repercussions worldwide in medium and long terms to undermine the credit-standing of OECD countries and to threaten the Euro system to generate investor panic for the sake of short term profits.

Any revised or new system must recognise if some EU members insist on maintaining large export surpluses then others must have sizeable external deficits. They cannot all aspire at the same time to export-led growth.

The Maastricht Rules should be elaborated to be made more intelligent, subtler and harder for the markets to analyse and play merry hell with! It does not follow that the answer is fiscal union or sameness within the Euro Area. And fiscal union should not mean aligning all tax and spending. It is not a sensible or workable basis for justifying cross-border financial guarantees. The proponents of more rigidity and fiscal alignment fail to see this course will require large fiscal transfers evey year between Euro Area member states.

President Nicolas Sarkozy called up Hu Jintao recently to ask if China would care to invest in the European Financial Stability Facility (EFSF), the Eur750bn fund. Sarkozy and Kanzler Angela Merkel are imagining China's US$3+ trillion in foreign exhange reserves as a source of ready cash. Should China say yes?

President Nicolas Sarkozy called up Hu Jintao recently to ask if China would care to invest in the European Financial Stability Facility (EFSF), the Eur750bn fund. Sarkozy and Kanzler Angela Merkel are imagining China's US$3+ trillion in foreign exhange reserves as a source of ready cash. Should China say yes?Of course China should participate because it adds to its mystique as a most successful economic power that is impervious to the crisis elsewhere. This is however not the true case. China is extremely vulnerable. Its economy is considerably smaller than official figures suggest and its economy is starting to nosedive beginning with a property collapse. China's banks are teetering on insolvency caused by funding gap and growing poor and non-performing loans and are only sustained by massive deposits from China's foreign currency reserves. China's industry is massively over-borrowed and very vulnerable to fall in export volume and or profits, already accutely modest.

Europe should not seek China's involvement in contributing to Euro Area crisis funds, or from OPEC countries' dollar reserves either. Such a course would be giving foolish testimony to EU insolvency and internal failure, which is not at all the true state of EU or Euro Area financial resources, which exceed that of China plus OPEC many times over!

The reason China cannot loan a few $ trillion is because its reserves are mainly committed by over $4 trillions to supporting China's domestic banks' balance sheets. Chinese households cannot add much to current deposits and are only permitted to borrow a third back while two thirds of household deposits and all of corporate deposits are lent to industry. There is nearly $5 trillion in loans to China's industrial borrowers in support of which the government has deposited $2 trillion with China's commercial banks and loaned them $2.5 trillions Yes, China has extra pocket change (generated annually from the trade surplus) and could support its trade with Europe more assiduously and politically by directly buying Euro Area bonds including those of the EFSF and or IMF, but probably by no more than a % of its annual trade surplus with the EU totalling perhaps $40 billions in 2011. But, this is a trivial and unnecessary, and for Europe's self-confidence and global prestige hugely damaging - EU's politicians need a wake up call to understand the realities they are playing with.

For quite good succinct discussion on the background see:

http://en.wikipedia.org/wiki/European_sovereign_debt_crisis